History of the Federal Reserve

The Federal Reserve has been in existence for over 110 years. While most Americans probably don’t know much about it, most have at least heard of it. People assume it has to exist because it has existed for their entire lives. So what exactly is the Federal Reserve, and what is its purpose? The Federal Reserve, also known as The Fed, is the United States’ central bank and is easily the most powerful in the world. The Federal Reserve is made up of three key entities: the Federal Reserve Board of Governors, a Federal agency in Washington, D.C.; 12 Federal Reserve Banks, spread across the nation; and 12 voting members from around the system who serve on the Federal Open Market Committee.

According to the Fed, it has five functions. First, and probably the most well-known, they set the nation’s monetary policy to promote maximum employment, stable prices, and moderate long-term interest rates in the U.S. economy. Secondly, they promote the stability of the financial system and minimize systemic risk. Next, it regulates banking institutions. It provides financial services to the U.S government. Lastly, it monitors and protects consumers’ credit rights. Another key element of the Federal Reserve Act is that it is to act as the lender of last resort. And when the lender of last resort actions fail, we get bailouts.[8]

Anyone familiar with the American economy over the last 100 years knows that the Fed has not been very successful in its purpose. So, how did we get to this point in our nation? Why is the Federal Reserve the most powerful central bank in the world? And why does the US have a central bank? To answer that, we will discuss the history of banking in the United States and the factors that led to the Federal Reserve Act of 1913.[2]

Early History of Banking in the United States

The Revolutionary War and the Bank of North America

To understand why we have a Federal Reserve in this country, we first must go back in history and understand our banking system. Going back to the Revolutionary War against Great Britain, the Continental Congress needed to find a way to finance the war. The Continental Congress turned to paper money. The person behind this drive was Gouvernor Morris. From 1775 on, they printed more and more fiat money. Before the war, the money supply was estimated to be $12 million. Then, from 1775 to 1779, Congress drastically increased the money supply. In five years, they added $225 million to the pre-existing $12 million. The result was rapid price inflation in terms of paper notes, and a corollary, accelerating depreciation of the paper in terms of species. And by 1781, the Continental paper currency, known as a Continental, became virtually worthless. The collapse of the currency led to the saying “not worth a Continental,” referring to the currency’s worthlessness.[2][9]

In 1781, the Continental Congress appointed Robert Morris to head the Finances. And by the Spring of 1781, Morris introduced a bill to create the first central bank in the history of the newly formed Republic. This new bank, the Bank of North America, would be the first fractional reserve commercial bank in the United States. It would be a privately owned central bank, modeled after the Bank of England. The money was to be grounded upon specie, but with a controlled monetary inflation, pyramiding an expansion of money and credit upon a reserve of specie. The Bank of North America opened its doors in 1782. It received the privilege of its notes being receivable in all duties and taxes to all governments, at par with specie. Additionally, no other banks were permitted to operate in the country.

The Bank of North America had a monopoly on issuing paper currency, and in return, it lent most of the money to the Federal Government to purchase public debt. The taxpayers would be on the hook for this. Soon after it began operations, the bank’s notes quickly became inflated in value relative to specie. The market’s lack of confidence in these bank notes led to their depreciation outside of Philadelphia, their home base. With Robert Morris’ power and influence slipping, he moved the Bank of North America from a central bank to a Pennsylvania state-chartered commercial bank. By the end of 1783, all the federal government’s stock in the bank, 5/8 of its capital, had been sold into private hands, and all the federal government’s debt to the Bank had been repaid. Thus ended the first experiment with a central bank in the United States.[2][1]

Thomas Jefferson vs Alexander Hamilton

Fast forward a few years, in 1789, the United States Constitution was ratified, establishing a more powerful central government than had existed under the Articles of Confederation. President Washington would be inaugurated that year. He would pick two cabinet members who would basically define the political party structure for the next 250 years.

Enter Alexander Hamilton, a young, intelligent, and ambitious gentleman with a particular vision for America. He wanted the United States to have a strong central government, similar to Great Britain, ruled by an aristocratic class. He would champion a central bank and believed that National debt was good to establish credit. Washington would appoint him as the Secretary of the Treasury. On the other side, we have Thomas Jefferson. Jefferson was extremely intelligent, more subtle than Hamilton, but also ambitious in his vision for the newly formed Republic. He envisioned the United States as an agrarian society with decentralized power, putting power in the hands of the common man. He was strongly opposed to central banks because he felt they favored merchants while working against farmers. Washington would appoint him as the Secretary of State.

Jefferson and Hamilton would clash on multiple issues, but economics was a major point of contention between them. Hamilton and his proponents would mold into the Federalist Party, while Jefferson and his allies would form the Democratic-Republican Party. Alexander Hamilton was a disciple of Robert Morris. In December of 1790, Hamilton submitted a report to Congress outlining his proposal for a National Bank. He used the Bank of England as the basis for his plan. Hamilton believed that a national bank could issue paper money, provide a safe place for public funds, act as the government’s fiscal agent, and collect tax revenue and pay government debt. Jefferson strongly disagreed. He believed that a National Bank would favor the financiers and merchants, who tended to be creditors. In contrast, farmers and plantation owners, who tended to be debtors, would be unfairly treated. He also thought that a national bank would undermine state banks by creating a financial monopoly.[2][5][10]

The Bank Bill passed Congress in February of 1791. Now all that was needed was for President Washington to sign the bill into law. Jefferson strongly urged President Washington to veto the bill. He wrote an opinion on the matter called “Opinion on the Constitutionality of the Bill for Establishing a National Bank, 15 February 1791.” Washington considered Jefferson’s opinion, and he gave Hamilton one week to rebut Jefferson. Hamilton, in response, wrote a lengthy 15,000-word opinion against Jefferson’s. Jefferson argued that the Constitution did not explicitly authorize the federal government to create a national bank. The phrase Jefferson focused on is “to make all laws necessary and proper for carrying into execution the enumerated powers.” While a national bank might make collecting taxes and other matters more convenient, convenience does not equate to necessity.

All these functions could still be carried out without a national bank. Hamilton argued the opposite. Since the Constitution did not prohibit the formation of a national bank, it was, in his opinion, constitutional. In Jefferson’s defense, this debate did come up at the constitutional convention, and the matter was struck down, so the need for a national bank was not necessary. In the end, Washington agreed with Hamilton and signed the Bank Bill into law. The First Bank of the United States was established in 1791 and had a 20-year charter. As Economist Murray Rothbard put it, “Hamilton would pave the way for unlimited expansion of federal power by maintaining that the Constitution ‘implied’ a grant of power for carrying out vague national goals.” Hamilton’s views would be solidified in 1819 when the Supreme Court made a ruling in McCulloch vs Maryland.[2][6]

The First Bank of the United States: 1791 to 1811

The First Bank of the United States was modeled after the Bank of North America. And not only that, Thomas Willing, the former president of the Bank of North America and Robert Morris’s good friend, would be made President of the new Bank. The Bank started with a capitalization of $10 million, of which, $2 million was owned by the government and $8 million by private investors, making it the largest financial institution and corporation in the United States. The bank’s share sale was the largest IPO in the country to date. However, many of the investors were foreign. And while they could not vote, this made Americans uncomfortable. Some of the bank’s functions included serving as the federal government’s fiscal agent, collecting tax revenue, making loans to the government, transferring government deposits, and paying the government’s bills. While the US Govt did not directly manage the bank, it did receive a portion of the profits. Additionally, the bank also operated as a commercial bank. Bank notes, also known as paper currency, usually entered circulation through the loan process. This First National Bank differed from today’s Federal Reserve because it did not set monetary policy like it does today. Also, it did not act as the lender of last resort for banks, as the Federal Reserve does today.[2]

The First Bank of the United States quickly inflated the money. Wholesale prices went from an index of 85 in 1791 to a peak of 146 in 1796, a 72% increase in just five years. Riding the coattails of this new paper currency was a flood of new commercial banks. In five years, the number of new banks went from four to 18. While the Democratic-Republicans took control of the White House and Congress in 1801, they did nothing to stop the National Bank. At that time, it was more the Moderates in the party than the Old Republicans who valued sound money. So the bank operated for 20 years unabated. During those 20 years, commercial banks grew to 117 by 1811. Finally, in 1811, when the charter was up for renewal, it was defeated by one vote. Vice President George Clinton cast the tie-breaking vote against the renewal.[2][9]

The Path to the Second Bank

The War of 1812

Shortly after the closure of the First National Bank, the United States would be dragged into a war with its former enemy, Great Britain, in 1812. Although the United States did not have a central bank, it still needed to find a way to finance the war. They relied on state banks to support the war. New England, however, was strongly opposed to war with Great Britain because it relied on trade and imports from the former motherland. But the New England banks remained conservative in lending, so the US did not finance much debt from them. However, they needed the manufactured goods in New England for the war effort. So what did the Federal Government do? They encouraged the formation of new banks in the Mid-Atlantic, Southern, and Western States. These new banks were reckless in their lending practices. And the Federal Government would use bank notes from these reckless and highly inflationary banks to purchase goods in New England. And what was the result of all of this? Well, as you might suspect, when the New England Banks called upon the other banks to redeem their notes in specie, the banks could not meet the demand because they did not have the specie to pay for all these bank notes. It was at this time that the Federal Government made a fateful decision. In August 1814, as banks outside New England faced failure, the Federal Government suspended specie payments to banks while they continued to operate, meaning they did not have to redeem the bank notes that promised gold and silver.

What was the result of the suspension of specie payments? It was a disaster for the US economy. In 1811, it is estimated that specie, gold, and silver in all banks totaled $14.9 million. And by 1815, that number dropped to $13.5 million, over a 9% decrease. On the flip side, banknotes and deposits in all these banks totaled about $42.2 million. By 1815, that number totaled $79 million, a 87% increase. But this doesn’t tell the whole story. Since the New England banks remained relatively sound, the inflation was more regionalized, hitting different areas of the country differently. Another point: the number of banks increased drastically, from 117 in 1811 to 246 by 1815. As you might expect, the suspension of specie payments and the inflation of the money supply did not yield good results. Wholesale prices increased on average by 35%. Inflation, depending on the city, ranged from 28% to 55%. With foreign trade cut off during the war, the prices of imported commodities rose by a staggering 70%. Suspension of specie payment lasted two and a half years, not ending until February of 1817, long after the war had ended.[2][9]

President James Madison and the push for a National Bank

The effects of the United States’ fiscal policy would be felt for years to come. With the suspension of specie payments from 1814 to 1817, as the money supply contracted, it led to a Panic in 1819 and then a depression. But before that, with James Madison in the Presidency, he advocated restoring the National Bank. As Murray Rothbard points out, “clearly, the nation could not continue indefinitely with the issue of fiat money in the hands of discordant sets of individual banks. There were two ways out of the problem: one was the hard-money path, which was advocated by the Old Republicans and, for their own purposes, the Federalists. Instead, the Democratic-Republican establishment in 1816 turned to the old Federalist path: a new central bank, a Second Bank of the United States.” While James Madison opposed the First National Bank, he supported the Second National Bank because he felt that it was necessary to finance the war with Great Britain. But after the peace treaty was signed, he withdrew his support. However, he would change his mind again, and in April 1816, President Madison signed the Bank Bill into law, establishing the Second Bank of the United States.

Then, Secretary of the Treasury Alexander Dallas was a proponent of the National Bank. Dallas, a wealthy Philadelphia lawyer, was close friends with Philadelphia merchant and banker, Stephan Girard. Girard was the largest stockholder of the First National Bank. Dallas and Girard managed to secure the position of President of the Second National Bank for their close friend, William Jones, another Philadelphia Merchant. The Bank opened its doors in Philadelphia in January 1817. The Second National Bank was similar to the First. It would be a private corporation with 1/5 of the shares owned by the Federal Government; it would issue a national paper currency, purchase a large amount of public debt, and receive deposits of Treasury Funds. The bank’s notes and deposits were to be redeemable in specie, and they were given quasi-legal tender status by the federal government’s receiving them in payment of taxes.

Like the First Bank, the Second Bank would act as the Federal Government’s fiscal agent, issue a common currency, and make direct commercial and individual loans. However, this last function would be controversial. Without any meaningful oversight, many of these loans were large, nonperforming, and made to insiders and friends. This left the bank close to bankruptcy just a few years into its existence. This was one of the concerns that Jefferson and his allies had; the Bank could be corrupted, funneling money to their political allies. One would think that the purpose of establishing a National Bank would be to crack down on state banks’ inflationary practices. However, Rothbard points out that that was not the case. Instead, they supported the state banks in their inflationary course with a deal the Second National Bank made in January 1817. While Congress was enacting the Bank charter, it passed a resolution of Daniel Webster, a hard-money Federalist, that would require, after 20 February 1817, the U.S. to accept, in payments for taxes, only specie, Treasury notes, National Bank notes, or state bank notes redeemable in specie on demand. In other words, no bank notes that could not be redeemed immediately in specie. However, the National Bank’s leadership met with representatives from urban banks outside of Boston. They agreed to issue $6 million worth of credit in New York, Philadelphia, Baltimore, and Virginia before insisting on specie payments on debt due from the state banks. Additionally, the Second National Bank and state banks agreed to support each other in any emergency mutually.[2][1]

The Second Bank of the United States

From the beginning, the Second National Bank was a disaster. They were very lenient on the required payment of its capital in specie, and the bank failed to raise the $7 million required to be subscribed in specie. In July 1818, the Second Bank held $2.36 million in specie and $21.8 million in notes and deposits, thereby severely inflating the money supply. Another issue that I alluded to earlier, the Second Bank of the United States partook in outright fraud. 3/5 of all loans were made in just two branches, Philadelphia and Baltimore. The Second Bank’s attempt to provide a national currency failed, too. The western and southern branches could inflate credit and bank notes, which they could then redeem in more conservative branches, such as New York and Boston, where these banks would be forced to redeem the inflated notes. So, in short, conservative banks would be stripped of specie, while risky banks could continue inflating the currency with no repercussions.[2]

Less than two years later, the Second Bank of the United States was in danger of going under. Over the next year, the Second Bank would be forced to conduct a series of contractions on loans and credit, especially in the South and West. This massive contraction of the United States’ money supply brought on a severe depression. This would be the first nationwide “boom-bust” cycle caused by the National Bank’s policy that everyone is familiar with today. The contraction in the Second Bank’s notes and deposits was massive! In June 1818, total notes and deposits totaled $21.9 million; one year later, that figure was $11.5 million, almost a 50% reduction!

Estimates for the total money supply went from $103.5 million in 1818 to $74.2 million in 1819. As you can imagine, this contraction had major consequences for the nation. There were several bank failures over the next three years, large drops in real estate values, declines in public land sales, and significant declines in export prices. Prices in general plummeted. These actions led to the saving of the Second Bank of the United States. However, as economist and historian William Gouge put it, “the Bank was saved, and the people were ruined.”[2][1]

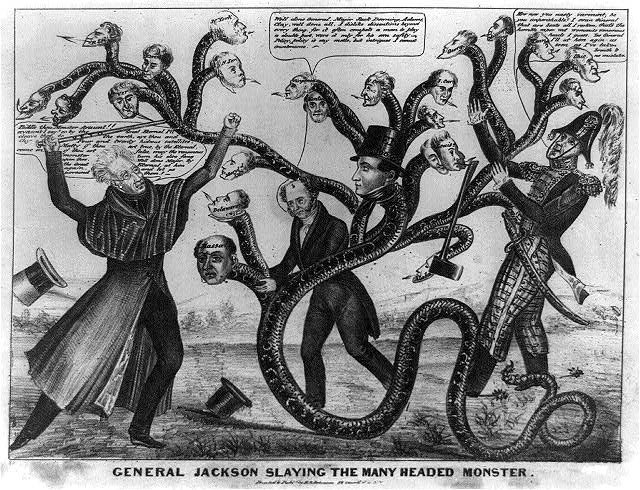

The depression after the panic of 1819 would linger for several years. Out of this experience with the First and Second National Banks would emerge the Jacksonian movement. Led by Andrew Jackson, the soon-to-be 7th President of the United States, the Jacksonians were hard-money advocates who wanted to do away with fractional-reserve banking, and specifically, to end the Second Bank of the United States. Some of his strongest allies would be Senator Thomas Hart Benton of Missouri and another future president and Jackson’s protégé, James K. Polk. Jackson was going to be in for the fight of his life, but if anybody could handle this fight, it was “Old Hickory.”[2]

Andrew Jackson and the Jacksonian Movement

President James Madison had signed the Bank Bill into law in 1816, establishing the Second Bank of the United States. However, the Federal Government’s suspension of specie payments led to a contraction in money in 1818, causing the Panic of 1819. Following this, the United States was thrown into the first-ever “boom-bust” cycle caused by the National Bank. What followed was a severe depression for the United States. Banks failed, real estate values plummeted, public land sales dried up, and export prices plunged.

Out of the ashes of this economic turmoil came the Jacksonian movement, also known as Jacksonian Democracy, a cause dedicated to the use of hard money, the elimination of fractional reserve banking, and the destruction of a central bank. The leader of this movement was Old Hickory himself, General Andrew Jackson. When Jackson assumed the Presidency, he would be engaged in what would become known as the Bank War. Jackson sought to crush the Second Bank of the United States. Jackson wasn’t alone. He had great allies. Senator Thomas Hart “Old Bullion” Benton of Missouri was in his corner. So was the one and only future President James K. Polk of Tennessee. Jacksonian economists Amos Kendall of Kentucky and Condy Raguet of Philadelphia were by his side, too. They were all converted to hard money and 100% reserve banking because of the experience of the Panic of 1819. Jackson was going to be in the fight of his life for the American people, going against Nicholas Biddle and the Second Bank of the United States. Biddle would have powerful connections that he would use to try to destroy Jackson.[2]

“Era of Good Feelings”

To discuss the rise of Andrew Jackson, we first must look at the reasons for Jackson’s rise to fame on the political scene. Flashback to 1800, when the political landscape consisted of two parties: the Federalist Party, led by Alexander Hamilton and John Adams. The Federalists were pro-central bank, high taxes, and a big central government. On the opposing side, we had the Democratic-Republican Party, led by Thomas Jefferson, James Madison, and others. In the 1800 election, John Adams, the first and only Federalist President, was defeated by Thomas Jefferson. From that point, it slowly dwindled into obscurity, becoming a minority party. It had a brief resurgence during the War of 1812, but by the 1816 election, it was essentially dead. This paved the way for the Democratic-Republican party to be the only major party in the political arena. This brief period became known as the “Era of Good Feelings.”

The party did start to become fragmented and this led to the election of 1824, which pitted four individuals from the party running for the Presidency: John Quincy Adams, Secretary of State under President Monroe; William Crawford, Secretary of the Treasury; Henry Clay, Speaker of the House of Representatives; and Finally, Andrew Jackson, former U.S. representative and Military hero from the Battle of New Orleans and essentially a populist candidate that had the support of the American People. With four candidates in the race, no one received a majority in the Electoral College or the popular vote; however, Jackson led the way with 99 electoral votes and 41.3% of the popular vote. Adams was in second with 84 electoral votes and 30.9% of the popular vote.

The decision went to the House of Representatives. Henry Clay came in fourth and was eliminated from the running. The election would now be between Jackson, Adams, and Crawford. However, Clay would throw his support behind John Quincy Adams. In return, Adams would appoint Clay as the Secretary of State. This deal would become known as the ‘corrupt bargain.’ Jackson was furious! This was the final straw for Jackson and the Democratic-Republican Party. This led Jackson and others to form a new party, known as the Democratic Party, the same Democratic Party that exists today. All Jackson could do now was wait for the 1828 election.[2]

Jackson’s 1828 Presidential campaign would essentially be a grassroots and populist movement. The election pitted Jackson against the incumbent President, John Quincy Adams. Jackson, still seething from the ‘corrupt bargain,’ would get his revenge, overwhelmingly securing the electoral votes with 178 to Adams’ 83 and taking 56% of the popular vote. While Jackson campaigned on several issues, we are only focused on his war with the central bank.[2]

The Bank War

Jackson strongly opposed the Second Bank of the United States, which he viewed as an institution that benefited the wealthy at the expense of the common man. Jackson had a comprehensive plan regarding money and banking. The first step would be to abolish the central bank. However, the bank’s charter was not set to expire until 1836. This led to a showdown between President Jackson and Nicholas Biddle, the President of the Second Bank of the United States. Among this showdown, Biddle had what he thought was an ace up his sleeve. Jackson was up for re-election in 1832, and Biddle thought that if Jackson opposed a re-charter, it would cause him to lose his reelection. Biddle, who had powerful allies in Congress, requested that Congress grant an early renewal of the charter. Senator Henry Clay baked the bill. The bill passed both houses of Congress, with approval of 107 to 85 in the House and 28 to 20 in the Senate.

The ball was now in President Jackson’s court. Would he risk reelection by vetoing the bill? Jackson placed his entire political career on the line and vetoed the bill! In his veto message, Jackson focused on three topics. Firstly, Jackson saw the national bank as an injustice, granting it a monopoly that favored the wealthy. Secondly, he saw the bank as unconstitutional. Lastly, the danger of the bank being dominated by foreign investors. About one-third of the bank stock was held by foreign investors.[2][7]

Would Jackson’s veto cost Jackson the 1832 election? No, Jackson cruised to reelection, earning 76% of the Electoral vote and 54% of the popular vote! Jackson’s gamble paid off! While Biddle had the Congress in his back pocket and the support of banks, speculators, industrialists, and elements of the press, Jackson had the people on his side. The common man! Now Jackson and his allies could get to work on destroying the central bank forever and putting America on the road to hard money.[2]

Dismantling the Second Bank

Soon after the election, Jackson removed the public Treasury deposits from the Bank of the United States and placed them in several state banks, which were soon labeled as ‘pet banks’ throughout the country. At first, using seven banks, but Jackson wasn’t interested in creating a class of privileged banks, so it was soon expanded to 91 banks. This was just a temporary solution; eventually, Jackson and follow-on candidates wanted to establish an Independent Treasury System. But Biddle wasn’t going to go down without a fight. He was going to make this as painful as possible for Jackson, and the American people would be cannon fodder. Biddle intentionally contracted the money supply, hoping to cause a panic as they had seen in 1819. He then hoped that Jackson would be blamed for this and that Congress would override his veto. Biddle’s contraction came at a bad time for Jackson and the American people. Business had been expanding due to the bank’s easy credit, which was dependent on it. Not to mention, the tariff came due at this exact time.

The impact was felt everywhere. Losses were sustained. Wages and prices dropped, unemployment increased, and businesses went bankrupt. Congress reconvened in December for the “Panic Session,” and Americans were in an uproar. As the pressure on Congress continued to mount, it looked like Biddle would defeat Jackson in this bank war. The public saw Jackson as responsible for this economic hardship. However, the tide began to turn, against Biddle and in favor of Jackson. The cause of this turn was none other than Biddle himself. Nicholas Biddle could not help but brag to Jackson and the American people about what he had done. And the people heard these boasts. Then, Governor George Wolf of Pennsylvania publicly denounced the Bank and Biddle. Support for Jackson and the Democrats swung firmly in his direction as the people and Congress turned against Biddle and the Second Bank of the United States.[2]

The Banking Interregnum: Free Banking, National Charters, and the Gold Standard (1836–1913)

“Free” Banking Era

America’s experience with its third national bank (counting the Bank of North America) was done at this point. How would the United States survive without a central bank? Jackson, having served his two terms, stepped away from the presidency and was replaced by one of his allies, Martin Van Buren.

After the Panics of 1837 and 1839, the Democratic Party became a strong proponent of hard money. From the 1830s through the Civil War, the United States was in what is known as the “free” banking period. It is important to note that this period in America, which is referred to as “free” banking, is not what is considered an actual free banking economy. A true free-banking economy would be, As Murray Rothbard describes it, as “a system where entry into banking is totally free; the banks are neither subsidized nor regulated, and at the first sign of failure to redeem in specie payments, a bank is forced to declare insolvency and close its doors.” The American “free” banking period was much different. For example, the government would allow the periodic suspension of specie payments when banks were overexpanded and were in hot water. Also, they were subject to several regulations and other things.[2][1]

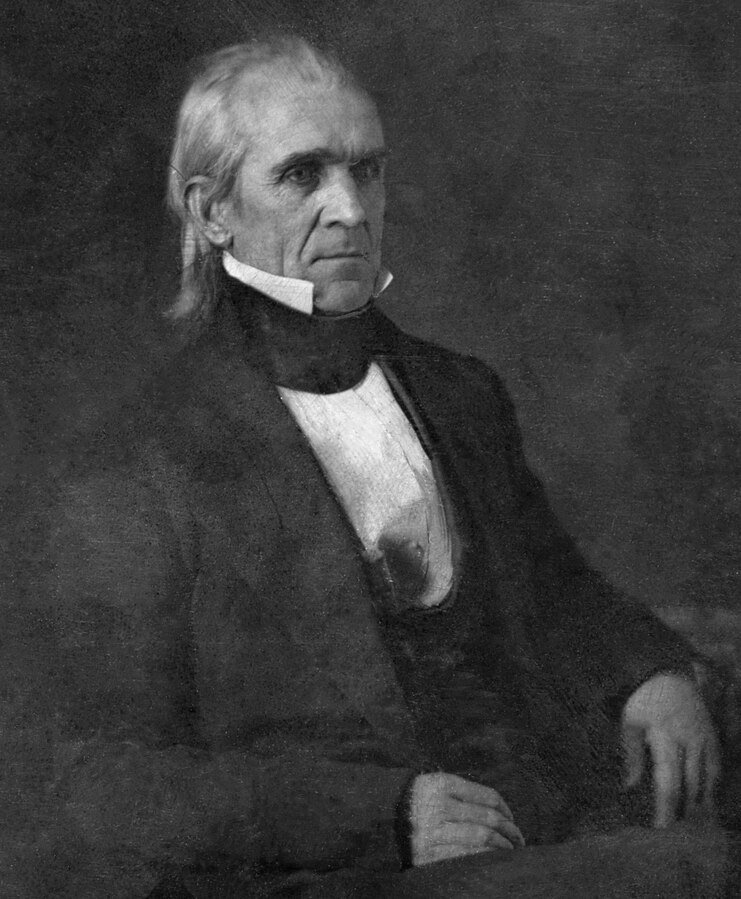

One accomplishment of the Democratic Party was the establishment of the Independent Treasury System. This was part of Jackson and the Democrats’ vision. Before it, the U.S. government had its funds held in state banks. In response to the panics of 1837 and 1839, President Martin Van Buren signed into law the Independent Treasury Act in 1840. This system would keep federal funds out of state banks and was managed by the Department of the Treasury. Unfortunately, this law was repealed in 1841, when the Whig Party took power. However, President James K. Polk would re-establish it when he signed the Independent Treasury Act of 1846. Unfortunately, the Independent Treasury System would be dismantled during the Civil War, and elements of it were formally abolished with the Federal Reserve Act of 1913.[2]

The Civil War, Greenbacks, and the National Banking System

The Civil War kicked off in 1861, with the secession of the southern states from the Union. Soon, the United States would be locked into four years of bloody war, pitting brother against brother. The U.S. Government faced severe financial constraints. The Confederate States would experience the same, if not worse, financial woes. How would both sides be able to fund this conflict? The period of the Civil War and the years that followed would completely alter the trajectory of the banking system in the United States. It would pave the way for the creation of the Federal Reserve.[2]

It is also worth noting that the Federal Government first experimented with an income tax during the Civil War. This was the first time in American history that the Federal government would have such a tax. For more on the Sixteenth Amendment, please check out my article and video, linked below. Returning to the issue of banking, the Civil War would set a dangerous precedent for the future of banking and ultimately pave the way for the Federal Reserve. Essentially, the Civil War would end the Federal Government and banking separation, and it would outlaw the issuance of state bank notes, thereby creating a new, semi-centralized, factional reserve banking system.[2][11]

Federal Expenditures and Monetary Challenges During the Civil War

The Civil War immediately bloated the Federal expenditures over the course of four years. In 1861, expenditures totaled $66 million, and by 1865, they reached $1.3 billion! And of course, by December of 1861, they would suspend specie payments, an old, detrimental trick used in the past. To help fund the war for the North, in 1862, Congress passed the Legal Tender Act, which authorized the issuance of paper money not backed by gold or silver. These notes were called “United States Notes,” but they were popularly known as “greenbacks.” This would set a dangerous precedent in the United States. Other than a brief period from 1814-1817, this was the first time the U.S. would experiment with irredeemable fiat currency.

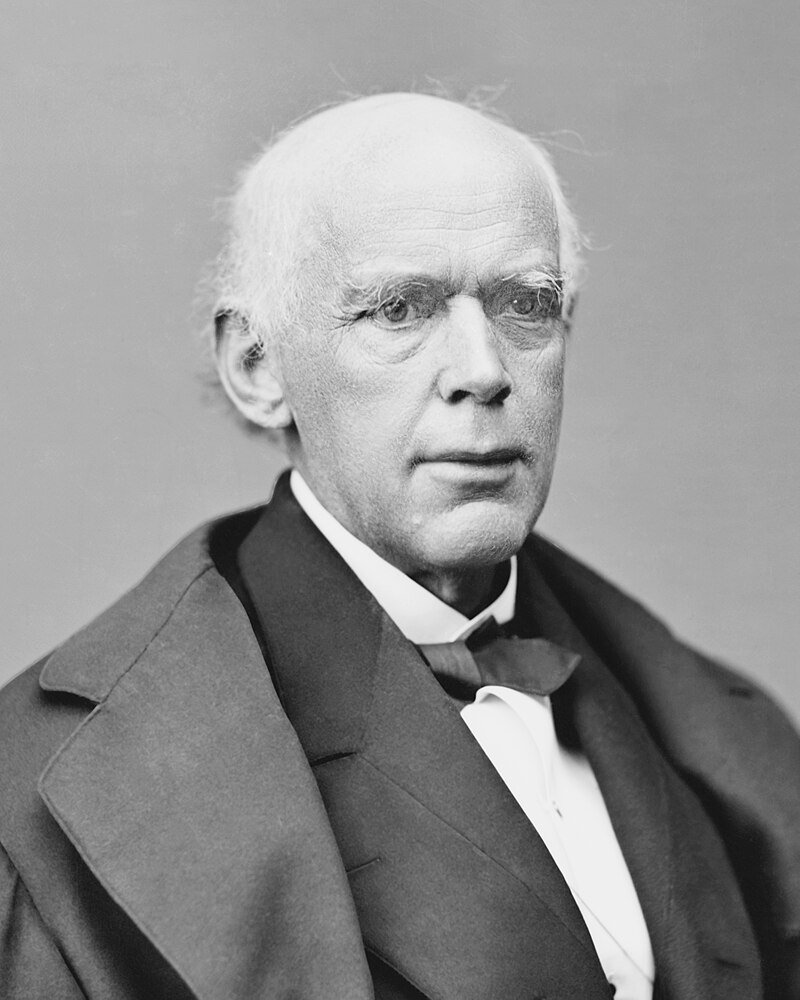

Secretary of the Treasury Salmon P. Chase strongly advocated for greenbacks. He said that they were an “indispensable necessity.” Ironically, eight years later, in 1870, Chase would serve as the Chief Justice of the Supreme Court. As Chief Justice, Chase and the Supreme Court would declare greenbacks unconstitutional in their ruling in Hepburn v. Griswold. More on that to follow.

What happened to Chase? Why did he suddenly change his mind? Like a lot of politicians, they see extreme measures in times of war as necessary, even if they violate the Constitution. This is important to note. With the creation of the Federal Reserve, the Federal Government will look for “emergencies” or endless wars to do things like violate the Constitution or print unlimited money. Getting back to Greenbacks, while the Federal government assured the American public that the greenbacks would be a temporary measure for a time of war, they were used until 1879, when the U.S. finally returned to notes backed by specie. The use of greenbacks was supposed to be only temporary and an emergency issue. However, they would do it again later that year, and again in 1863.

Greenbacks peaked in 1864 with $415.1 million. As always happens when you print fiat money, the greenbacks lost their value. The Treasury Secretary tried to place the blame on the gold speculators. He fought this depreciation on several attempts. And finally, he made one last attempt, which crushed the gold market. The gold market was a complete disaster. Chase would be forced to resign in June 1864. Total Money supply of the country skyrocketed, from $745.4 million in 1860 to $1.773 billion in 1865! Wholesale prices would increase substantially as well.[2][9]

National Banking System

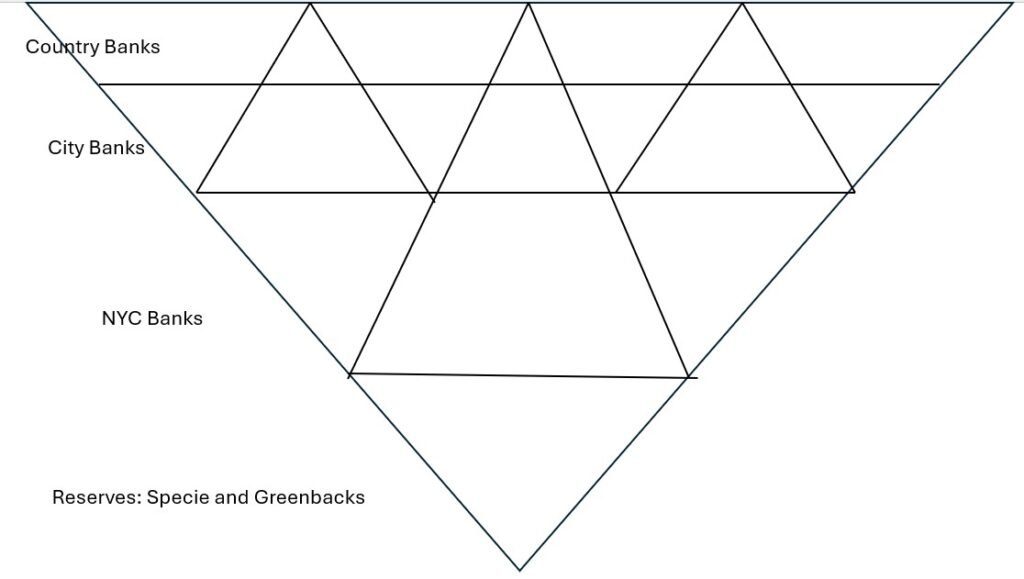

To get a little understanding of how this banking system worked, the system started with what were called the “Central Reserve City” Banks, which were only in New York. Above them were the “Reserve City” banks, which were banks in cities with over 500,000. On top of those banks were the country banks. Down the road, state banks would be added to this structure. Murray Rothbard describes the structure as an inverted pyramid, with the New York City Banks below the others, as depicted in the picture below. Banks were required to hold reserves based on bank type and were allowed to pyramid the entire banking structure atop a few Wall Street banks.[2][1]

While the Civil War ended in 1865, the National banking system was going nowhere. On top of that, the Greenbacks would hang around until 1879. Still, in 1865, state banks refused to join the national banking system voluntarily. Congress punished them in March 1865 by placing a prohibitive 10% tax on their bank notes. The national banks now had a legal monopoly. This shocked the state banks, their numbers dwindling from 1,466 in 1864 to 297 in 1866. However, state banks would gradually return and essentially join the national banking system. They became the fourth layer of Murray Rothbard’s inverted pyramid. This would intensify the inflation.[2]

The Greenback Problem

With the end of the Civil War, the United States was strapped with depreciated inconvertible greenbacks and heavy public debt. How would the Federal government get rid of these greenbacks? When would specie payments resume? Enter the industrialists, the backbone of the 19th-century Republican Party. These industrialists advocated for the continuation of greenbacks and opposed resumption and any contraction of money to prepare for specie resumption. Why would they do that? Because fiat money and inflation benefit the wealthy. They continue to get rich while the lower and middle classes lose wealth.

These industrialists were headed by Pennsylvania iron and steel manufacturers and the railroad companies. Also on board were the gold speculators. Manufacturers wanted the cheap credit while gold speculators wanted higher gold prices. For the railroads? Well, they were heavily in debt, and an inflated money supply would debase the dollar and, by extension, their debt. It was so bad that one Wall Street speculator, Richard Schell, wanted a canal dug from New York to San Francisco. The railroad building at this point in American History had spun out of control. Which leads us to the Panic of 1873.[2]

During this time, the money supply leveled off. It did not contract; it merely leveled off, causing the panic. Another major factor was the railroad industry. The railroads had overextended themselves, riding the tide of vast government subsidies and bank speculation. Jay Cooke and his Northern Pacific Railroad company went bankrupt in 1873, leading to the panic. The panic led to a large number of bankruptcies of overinflated banks. It is worth noting that during this time, greenbacks were still legal, which leads us into an interesting story.[2]

Chief Justice Salmon P. Chase

After Salmon P. Chase served as the Treasury Secretary; he would later be appointed Chief Justice of the Supreme Court. In dealing with the issue of greenbacks, it was split mainly along party lines. Republicans favored them, while hard-money Democrats opposed them. Before 1870, state courts addressed the issue of greenbacks. Every Republican judge, except one, ruled that they were constitutional. However, all but two of the Democratic judges would strike them down as unconstitutional. In 1867, the issue reached the United States Supreme Court, and they ruled on it in February 1870 in the case Hepburn v. Griswold. Salmon Chase, who just a few years earlier was an advocate for greenbacks to fund the war, would strike down greenbacks with a 5-3 decision, declaring them unconstitutional.

The industrialists and the Republican Party were struck a severe blow. President Grant and the railroads were upset by this ruling. The railroads accumulated a lot of long-term debt, which would now have to be repaid with more valuable gold. What did President Grant do to combat this ruling? Well, lucky for him, two justices on the Supreme Court retired shortly after. Grant appointed two republican judges in their place. Not only were they republican justices, but they were two former railroad lawyers, whose political views were no big secret. In May of 1871, the Supreme Court reconsidered this ruling, and in a 5-4 decision in Knox v. Lee, they reversed the court’s previous decision. The railroads were saved![2]

The Gilded Age

From the period after the Civil War, the resumption of specie would be a hot topic. Finally, in 1875, the United States would pass the Resumption Act. However, it would be another four years before the Federal Government would implement the Resumption Act. From 1879 on, the United States would be back on a gold standard, for the first time since before the Civil War. At this point, the National Banking System was fully entrenched in the American financial system and was not going anywhere. And with the return to the gold standard, the United States would see one of the most expansive times in history. Murray Rothbard points out that while prices fell during both the 1870s and 1880s, wages grew during the 1880s when the US was on a gold standard. During the greenback era, prices fell, but so did wages.

The 1880s and into the 1890s would see some of the greatest wealth and expansion in American economic history. And it wasn’t just the industrialists and manufacturers who were getting rich; the farmers also had an excellent decade, with growth in productivity and output. Yes, the manufacturers grew at a faster rate, but the farmers also saw substantial growth during this period. While times were good at this time, it is important to point out that, just because the US was back on a gold standard, it was far from a free-market money system. The National Banking Act had created somewhat of a banking cartel in the United States by granting the privilege of issuing bank notes to a few large national banks and penalizing state banks. Right around the turn of the 20th century, a political transformation would affect the American banking system for good.[2][1][9]

Realignment of the Political Parties

Since the days of Andrew Jackson, the Democratic Party had always been hard money libertarians, while the Republican Party had always been the party of big business and cheap money. Around 1896, the parties were about to change. With the Democratic nomination of William Jennings Bryan, the populist movement began to influence the Democratic Party, causing it to shift from its laissez-faire approach to more inflationary policies. Meanwhile, the Republicans saw this as an opportunity, and in 1896, they had McKinley pledge support for a gold standard. Regardless, gone were the days of hard-money democrats fighting for the liberties of every individual. The political landscape was about to shift drastically with the Progressive movement in the early 20th century.[2]

Also in the late 19th century, the political parties were experiencing a political shift. The Democratic Party, founded by hard-money libertarians such as Andrew Jackson, experienced a populist movement led by William Jennings Bryan. This movement led the party away from its hard-money origins. Bryan was against the gold standard and favored a policy that was known as “free Silver.” He wanted the US to mint unlimited silver because he believed that easy money benefited the common man. The hard-money Democrats’ power diminished considerably until they were nothing more than a footnote in the pages of history.

The Republicans, however, seeing an opportunity in 1896, adopted a gold standard, secured the backing of big business, and swept McKinley into the White House. While the Republicans adopted a stance in favor of the gold standard, they were still pro-greenbacks. And McKinley had the backing of banking giant JP Morgan. Morgan, while a proponent of the gold standard, wanted an elastic currency controlled by the banks. So while the Republican Party was the supposed party of the gold standard, this was a far cry from the days of the Jacksonian Movement. Morgan would play a pivotal role in pushing a central bank on the United States.[2][3]

Wall Street’s Push for a Central Bank

Indianapolis Monetary Commission

To achieve an elastic currency, Morgan and the bankers planned to start a reform movement to address the problem of inelasticity and gradually move toward a central bank. The only problem with this is that the public would never support the most powerful banker in America calling for reform. His solution was to disguise it as a grassroots movement, made to look spontaneous and started by small business owners. The plan would start with a convention in Indianapolis in 1897, making it appear as though it had Midwest origins. This was attended by tons of bankers and businessmen. Some other attendees were Henry C. Payne, a Republican Party leader, and George Foster Peabody, a powerful American Banker. This convention urged President McKinley to continue the gold standard and create a new system of elastic bank credit. How did Morgan’s plan fare? In general, it worked. The public generally saw this event as a spontaneous grassroots effort started by small businessmen.

At the convention, the bank reformers drafted a bill to present to Congress that would establish a National Monetary Commission. It passed the House, but it died in the Senate. While the bill may have failed, the movement had momentum. Next, the committee appointed a new Indianapolis Monetary Commission (IMC), comprising several prominent people, including bankers, businessmen, and professors. One of the most important members of this commission was University of Chicago Economics Professor James Laurence Laughlin. He will play an important role in this reform movement. We will discuss later the role academia would play in the push for a central bank. It should be noted, too, that business tycoon John D. Rockefeller essentially founded the University of Chicago, providing its initial endowment.[2][3]

The IMC would hold a second convention in 1898. Their purpose, according to former Secretary of the Treasury Charles S. Fairchild, was to mobilize the nation’s leading businessmen into a mighty, influential reform movement. Following the convention, the commission would release its preliminary report. Not only did they call for more banknotes, but they also openly called for a central bank to issue them. The banking reform movement was well underway and appeared grassroots. It appeared as though the nation was calling for a central bank, but in reality, it was the big bankers who were backing this movement.[2][3]

Gold Standard Act of 1900

To codify the gold standard, the reformers would need to pass a law. However, they would need to wait until after the 1898 election because gold proponents were not in control. They gained control in that election cycle, and in 1900, McKinley signed the Gold Standard Act. This law provided a single gold standard and diminished silver’s power, no longer redeemable for gold. The bankers had accomplished their first step toward banking reform, but it seemed they were still far from establishing a central bank.[2]

On a side note from the push for banking reform, the United States was also entering a new era of imperialism. With the Spanish-American War, the United States crushed the Spanish Empire with ease, and it officially entered the age of imperialism, claiming territories in the Caribbean and the Philippines. This new venture into imperialism would shape the United States’ approach to economics and monetary policy. This is a topic that could have its own article, so we are not going to discuss it today. Still, it is essential to know that the United States was entering a new age of Imperialism, much like the European powers had been practicing for years.[2]

President McKinley’s Assassination and TDR

Back to the banking reform movement. The push toward a central bank continued with the proposed Fowler Bill. This bill would further expand the scope of national bank notes to include broader assets and other functions, but the country’s banks defeated it. Senator Nelson W. Aldrich of Rhode Island submitted the Aldrich Bill, a more modest Version than Fowler’s, that would allow New York’s large banks to issue emergency currency, but it too was defeated. Then, in 1901, there was a significant event in America: the assassination of President McKinley. Theodore Roosevelt would assume the presidency. This presidential shift also meant a shift from a Rockefeller-dominated administration to a Morgan-dominated administration.[2][3]

The push for a central bank continued in the early years of the 20th century, and in 1906, a banker named Jacob H. Schiff, head of the Wall Street investment bank Kuhn, Loeb & Company, gave a speech before the New York Chamber of Commerce. Schiff argued that the United States needed an elastic currency and urged the Committee on Finance to draft a plan for a modern banking system to support it. The finance committee of the New York Chamber did just that. However, when it got to the bank reformers, they denounced it. Frank A. Vanderlip, President of the National City Bank of New York, set up a committee to investigate currency reform. When the committee delivered its report in October 1906, it openly called for a central bank. The bank reform movement continued to pick up steam. However, it seemed to be stuck in neutral for the time being.[2][3]

Early Twentieth Century Tactics

The Panic of 1907

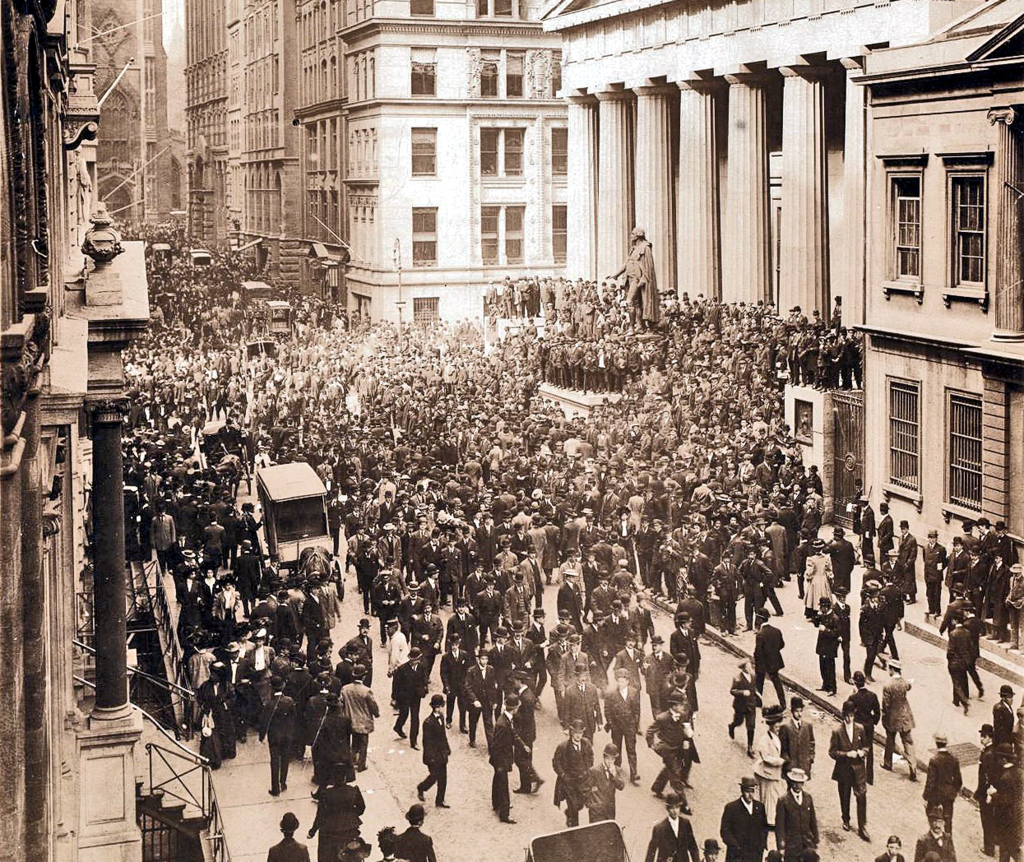

While bank reformers pushed for currency reform and a central bank, what they needed was an event to justify what they were calling for. They had such an event in 1907, with the Panic of that year. The Panic of 1907 was a severe financial crisis. Not only was there a contraction, but the government authorized major banks in New York and Chicago to suspend specie payments. This was just the type of crisis the bankers needed to push their agenda for a central bank. Just like the panics of 1873, 1884, and 1893, the Panic of 1907 was triggered by currency drains during periods of prosperity, when banks had loaned out so many loans that they had no reserves at all. Bankers and businessmen alike quickly called for a central bank, an institution that would regulate the economy and be a lender of last resort. A bank that could bail out these banks when they faced financial trouble.[2][3]

Academia Support

Another important aspect of the banking reformers’ plan to advocate for a central bank was to gain the support of academia. If they could get supposed experts on board with a central bank, that would help sway the public to their plan. Because what better way to gain public support than to enlist the experts of America’s trusted institutions? First, we’ll focus on Columbia University. Following the Panic of 1907, Columbia held three symposia from 1907 to 1908. In these, they openly called for a Central Bank. Professor Edwin Seligman led off with his opening address. The professor baselessly claimed that the panic was only moderate because of the growth of industrial trusts and that a horde of small businesses could not do the same. Also speaking was Frank Vanderlip, an American banker who would later serve as president of the National City Bank of New York. He claimed that the panic was the result of decentralized banking. The last speaker at the first symposium was a German-born American banker named Paul Warburg, who is sometimes called the father of the Federal Reserve. He would become a partner at Kuhn, Loeb, & Co. He also had a connection to the Rothschild dynasty of Europe.[2][3]

Another way the bank reformers secured the backing of the Universities was through a special educational fund of $5 million, which went to three universities: Harvard, Princeton, and, of course, the University of Chicago. All three had been recipients of large endowments from the financial and industrial worlds. Before this time, the study of economics was not a very prestigious endeavor. But now it has started becoming a more prestigious and acceptable field. So it wasn’t difficult to find hungry professors who would promote banking reform in return for a grant or an appointment. So, as mentioned earlier, one key academic that these captains of industry recruited was none other than James Laurence Laughlin, head of the political economy department at the University of Chicago and editor of its prestigious Journal of Political Economy. And while he was supposedly an orthodox laissez-faire theorist, he was the leading academic advocate for banking reform. Now that the bank reformers had academia on board, they were ready to push their agenda to the public. Because what better way to get the public on board than to have the supposed “experts” pushing for a central bank and an elastic currency?[2][3]

American Media Support

At this time, the Bankers were successful in getting academia on board; they were missing one piece to help push their objective. And that was the American press. They needed them to help drive the narrative home to the public. Kicking this off for the bankers was the Wall Street Journal, which on September 22, 1909, published a 14-part series titled “A Central Bank Issue.” Many other news organizations also got on board, calling for banking reform and advocating for a central bank.[2][3]

Meanwhile, in 1909, Paul Warburg continued his campaign for a central bank. He gave a famous speech at the New York YMCA on “A United Reserve Bank for the United States.” In this speech, he described the structure of the proposed bank. But it was basically just a blueprint of the German Reichsbank, a bank he was all too familiar with as a German. He pushed baseless statistics, saying that 60%of banks favored a central bank as long as Wall Street didn’t control it. And he insisted that it be called a Reserve Bank and not a central bank. Make no mistake, the purpose behind this was to pull the wool over the public’s eyes on what the bankers wanted. And who was Warburg’s biggest cheerleader? It was none other than Columbia professor Edwin R.A. Seligman. Additionally, the NMC flooded the public with opinion pieces in support of a central bank. Bankers, using academia and the media, had successfully pushed the narrative that all experts, bankers, and businessmen believed a central bank was the only way forward for the United States. It was now 1910, and it was time to act.[2][3]

Final Push for the Federal Reserve Act

Jekyll Island and the Aldrich Bill

What happened next would be an event that would completely alter world history. In 1910, six powerful men met in secret at an undisclosed location on Jekyll Island, Georgia. What would come of this meeting is what G. Edward Griffin calls The Creature From Jekyll Island, as detailed in his book of the same name. The six men making this voyage were Nelson Aldrich, United States Senator from Rhode Island; Abram Piatt Andrew, the Assistant Treasury Secretary, Frank A Vanderlip, President of the National Citibank of New York; Henry P Davison, senior partner of the JP Morgan Company; Paul Warburg, partner at Kuhn, Loeb and Co and representative of the Rothchild banking dynasty of Europe; and lastly Benjamin Strong, head of the JP Morgan’s bankers, trust company. In the United States, two groups held most of the wealth and power: the Morgans and the Rockefellers. In Europe, it was the Rothschilds. These six people represented one-sixth of the world’s wealth.[3]

What went on at this get-together, which brought together the wealthiest from America and Europe, is unknown. It wasn’t an official government meeting, so there are no records of what was discussed. But what came from it would be their blueprint for what they wanted central banking to look like in the United States. Senator Aldrich would submit the first draft of the Jekyll Island Plan to the Senate. It would become known as the Aldrich Bill. The key components of this bill were that it called for a central bank. It was similar to the old Bank of the United States, but with more power. And one key addition would be the power to create the national currency. While the bank reformers had the plan for a central bank ready, they made one fatal error. At Jekyll Island, there was disagreement on what to call the bill. Senator Aldrich, being an egomaniac, wanted his name attached to it. However, Paul Warburg, knowing that the Alrich name was associated with Wall Street, wanted to name it something like the “Federal Reserve Bill,” purposely avoiding terms associated with a central bank. In the end, Aldrich won out and had his name attached to it. But Warburg was right, the bill died a quick death. It didn’t even come to a vote because it had the name Aldrich attached to it. Then, in 1910, Republicans would lose the House. The Republican Party was much more open to the banker’s plan of banking reform and a central bank. And then in 1912, they would lose the Senate and the Presidency. A bill for the central bank would have to wait.[3][2]

Woodrow Wilson’s Election

In 1912, President Taft looked well on his way to reelection. However, Taft would not support the Aldrich Plan. He wasn’t opposed to the central bank itself, but he wanted more government control and less banker control. This infuriated the captains of industry. They needed to get rid of Taft. Their solution? Have Teddy Roosevelt run as a third-party candidate to derail Taft’s reelection bid. They didn’t expect Roosevelt to win; they just needed Taft to lose. And if Democratic nominee Woodrow Wilson won the election, that was ok, they could work with him. While the Democratic platform plank was “we oppose the so-called Aldrich Bill or the establishment of a national bank,” Wilson was an ally of the Wall Street banks. Wilson had close ties with executives of Rockefeller’s National City Bank. Cleveland Dodge and Cyrus McCormick had both been classmates of Wilson’s at Princeton University. And when Wilson came back to his alma mater as a professor in 1890, these two bank executives were University trustees. These two men had a major role in Wilson becoming the President of Princeton University. So Wilson was indebted to these men.[3][2]

With the Aldrich Plan’s demise, the Democrats were working on their own proposal. The man responsible for the Democrat proposal was Congressman Carter Glass of Virginia. Also, the Democratic Chairman of the House Banking and Currency Committee, Glass, was tasked to write the Democratic version of a bank bill. Although he was not familiar with banking, Washington and Lee University professor Henry Parker Willis helped him. And Willis was the protégé of none other than Professor Laughlin. Glass had several objections to the Alrich Bill, most importantly that it gave too much power to New York banks and lacked government control. So Glass introduced his bill and soon merged it with a similar measure sponsored by Senator Robert L. Owen, becoming known as the Glass-Owen Bill. How did this bill differ from the Aldrich Bill? Essentially, nothing. All of the key aspects of the Aldrich Plan remained in the Glass-Owen Bill, with some minor tweaks. The Glass-Owen Bill was specifically designed to differ from the Aldrich plan only in non-essential items, giving it the appearance of a new and improved bill, separate from the Aldrich plan.[3][2]

The bill was debated in Congress for several months. And while issues of the bill were debated, such as whether there should be 4, 8, or 12 regional banks, or whether the government or bankers should control the central bank, there was little resistance to the idea of a central bank. What happened to the Democratic Party of Andrew Jackson? Were there no more hard-money democrats? In 20 to 30 years, the democratic party shifted drastically.[2]

William Jennings Bryan’s Resistance

However, there was democratic resistance to the bill, not for the reasons a student of American history might expect. William Jennings Bryan was a highly influential member of the Democratic Party. As mentioned earlier, Bryan was a populist, and they believed that an elastic currency would benefit the common man. But the progressive wing did oppose the bill because of a lack of government control. So that would require a compromise.

Bryan had two demands for the bill to pass: The Federal Reserve notes must be treasury currency and guaranteed by the government, and second, the governing body must be appointed by the president and approved by the Senate. That’s it. Not much of a resistance. The bank reformers actually expected this. They suspected that they would eventually have to concede this to get the bill passed anyway. It is possible they intentionally left it out to create the illusion that they were compromising during the bill’s passage.[2][3]

While Congress debated the bill throughout 1913, it was finally ready to vote on the measure in December of that year. On December 22nd, the House approved the Federal Reserve Act of 1913 by a vote of 298 to 60. Then, on December 23rd, the Senate voted in favor of it 54 to 34, and it passed with relative ease. Here are the key takeaways of the bill: it created a centralized banking system with 12 regional banks across the country, managed by the Federal Reserve Board in Washington, D.C. The system was designed to create a safer and more flexible monetary framework for the nation while serving as a lender of last resort for banks. Its purpose was to prevent financial panics. Additionally, it granted the Federal Reserve the authority to influence both the money supply and interest rates. Lastly, it introduced an elastic currency, a money supply that could expand or contract based on economic needs.

It should be noted that the Federal Reserve Act has been amended over 200 times since 1913, one notable example being in 1977, which required the board and Federal Open Market Committee to promote maximum employment, stable prices, and moderate long-term interest rates. But we won’t get into all of the modifications.[8]\

What the Federal Reserve has Done for Americans

Since 1913, the United States has had a central bank, though it is disguised by the name “Federal Reserve.” And it does not appear that the United States will abolish it anytime soon. America has come a long way from the days of Andrew Jackson and his battle against a central bank. What happened to the Americans who were opposed to a central bank? Why have we become so complacent?[4]

Recessions and Inflation since 1913

So, what has happened since the passing of the Federal Reserve Act? Has it achieved its objective of preventing panics and providing economic stability? Well, since its inception, the Federal Reserve has presided over crashes in 1921 and 1929, the Great Depression from 1929 to 1939, and only to be rescued by the outbreak of World War II, the dot.com bubble in the early 2000s, the housing market crash in 2008 and the follow-on Great Recession, massive inflation in the 1970s and the early 2020s, and finally a recession in 2020. That is quite a record. Any other organization would have to close its doors with that track record.

From 1913 to 2025, the U.S. dollar has lost 97% of its value. What $100 would buy in 1913 would cost $3,187.93 today, according to officialdata.org. And this is going off the official CPI inflation numbers. It is probably much worse than the Bureau of Labor Statistics is letting on. Compare that from 1789 to 1912. According to officialdata.org, $100 in 1789 would be worth $110.23 in 1912, that is only a 10% increase over 123 years. Yes, the United States experienced inflation throughout that time period. Still, the beauty of a free market, hard-money society is that the price of goods will naturally drop due to technological advances. The natural state of the free market is deflationary. Therefore, over the long run, inflation would even out.[4][9][12]

Transfer of Wealth and Bailouts

Another concern raised by the Federal Reserve is the massive transfer of wealth. Just recently, in 2021 to 2022, with the COVID spending, we saw the largest transfer of wealth in human history. The world’s ten richest men more than doubled their fortunes, going from $700 billion to $1.5 trillion! While lower and middle-class Americans received a $1200 check, the 1% were getting even richer, thanks to the Federal Reserve. And of course, there are bailouts. Banks are being bailed out for taking risks that didn’t pan out. As Ron Paul calls it: privatized profits and socialized losses, meaning that if the bank profits, it reaps the rewards from those risks. However, if they take risks and lose money, then the taxpayer is on the hook for bailing out the bank. So the banks get all the rewards and none of the risk. Who wouldn’t want that deal? It would be like if I were a gambling addict and made insanely risky bets, but if I lost, the taxpayers had to pay my debts. As G. Edward Griffin points out in The Creature from Jekyll Island, “the name of the game is bailouts. The banks want a bailout, that is the inevitable goal, to shift the losses from the banks to the taxpayers.”[3][4]

So, what will the future of banking look like in the United States? Will the Federal Reserve ever be abolished? It has already far surpassed both the First Bank and Second Bank of the United States in both power and longevity. Will we ever get a modern-day Andrew Jackson to launch a crusade against the Federal Reserve?

Endnotes

- Rothbard, M. N. (1983). The Mystery of Banking. Richardson & Snyder. Available at: https://mises.org/library/book/mystery-banking (Accessed August 10, 2025).

- Rothbard, M. N. (2002). A History of Money and Banking in the United States: The Colonial Era to World War II. Ludwig von Mises Institute. Available at: https://mises.org/library/book/history-money-and-banking-united-states-colonial-era-world-war-ii (Accessed August 10, 2025).

- Griffin, G. E. (1994). The Creature from Jekyll Island: A Second Look at the Federal Reserve. American Media. Available at: https://www.amazon.com/Creature-Jekyll-Island-Federal-Reserve/dp/0912986212 (Accessed August 10, 2025).

- Paul, R. (2009). End the Fed. Grand Central Publishing. Available at: https://www.grandcentralpublishing.com/titles/ron-paul/end-the-fed/9780446568180/ (Accessed August 10, 2025).

- Hamilton, A. (1790, December 13). Report on a National Bank. Founders Online, National Archives. https://founders.archives.gov/documents/Hamilton/01-07-02-0229-0003 (Accessed August 10, 2025).

- Hamilton, A. (1791, February 23). Opinion on the Constitutionality of a National Bank. Founders Online, National Archives. https://founders.archives.gov/documents/Hamilton/01-08-02-0060-0003 (Accessed August 10, 2025).

- Jackson, A. (1832, July 10). Veto Message Regarding the Bank of the United States. Avalon Project, Yale Law School. https://avalon.law.yale.edu/19th_century/ajveto01.asp (Accessed August 10, 2025).

- U.S. Congress. (1913). Federal Reserve Act, Pub. L. No. 63-43, 38 Stat. 251. Available at: https://www.federalreserve.gov/aboutthefed/fract.htm (Accessed August 10, 2025).

- U.S. Bureau of the Census. (1949). Historical Statistics of the United States, 1789-1945. U.S. Government Printing Office. Available at: https://www.census.gov/library/publications/1949/compendia/hist_stats_1789-1945.html (Accessed August 10, 2025).

- Hamilton, A. (1790, December 13). Report on a National Bank. Founders Online, National Archives. https://founders.archives.gov/documents/Hamilton/01-07-02-0338-0003 (Accessed August 10, 2025).

- U.S. Congress. (1909). Congressional Record: Proceedings and Debates (SJ Res 40). Available at: https://www.govinfo.gov/content/pkg/GPO-CRECB-1909-pt4-v44/pdf/GPO-CRECB-1909-pt4-v44-21.pdf (Accessed August 10, 2025). [Note: This resolution relates to the 16th Amendment proposal for income tax, as mentioned in the article.]

- Bureau of Labor Statistics. (2025). CPI Inflation Calculator. U.S. Department of Labor. Available at: https://www.bls.gov/data/inflation_calculator.htm (Accessed August 10, 2025). [Added as fit for inflation stats.]

- Federal Reserve Bank of St. Louis. (2025). Economic Data (FRED) – U.S. Dollar Purchasing Power. Available at: https://fred.stlouisfed.org/ (Accessed August 10, 2025). [Added for additional economic data reference.]